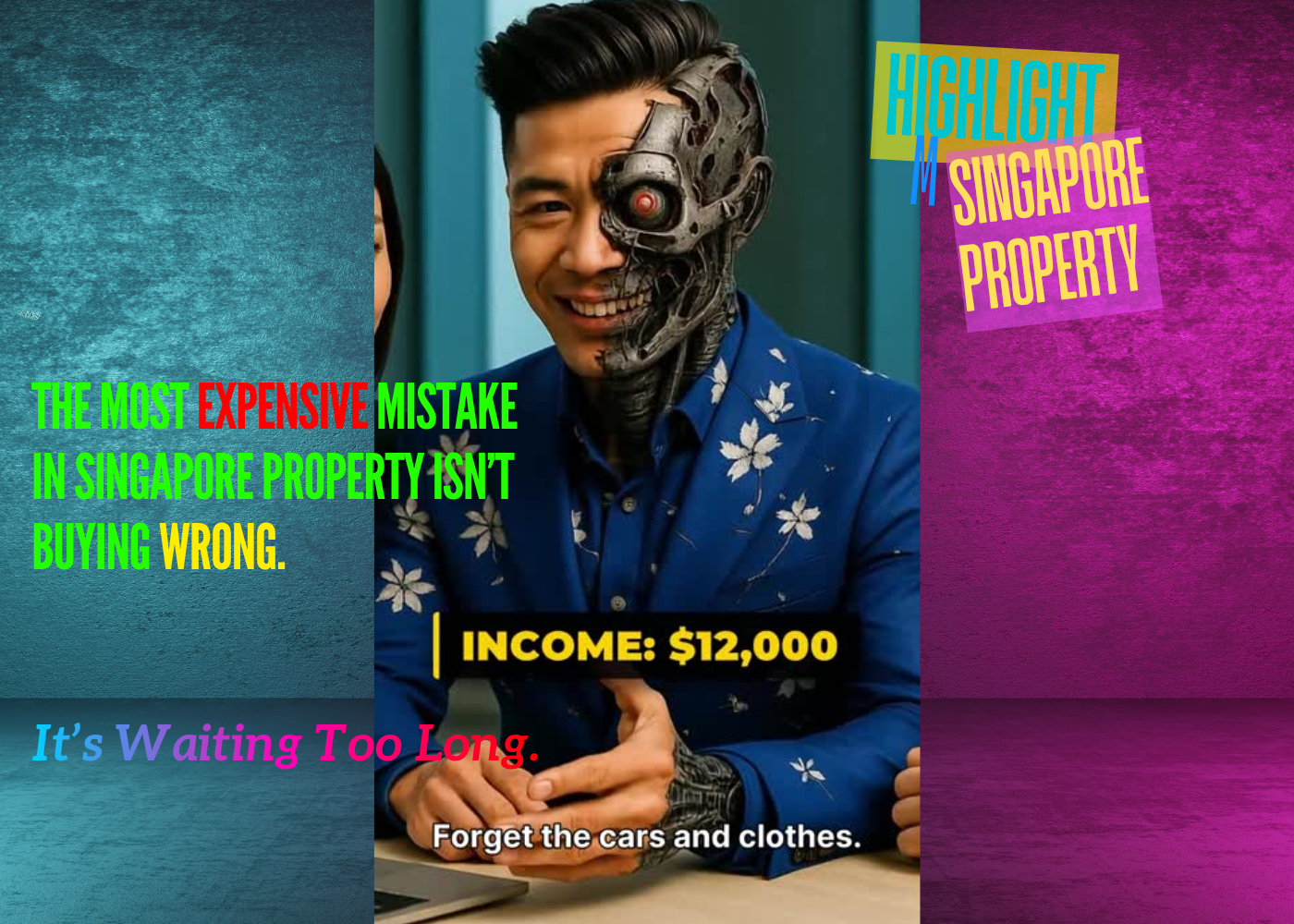

The Most Expensive Mistake in Singapore Property Isn’t Buying Wrong. It’s Waiting Too Long.

Most people believe waiting makes them smarter.

Wait for rates to drop. Wait for prices to stabilise. Wait until the “perfect unit” appears.

It sounds responsible.

It feels logical.

But in Singapore property, waiting is not neutral.

Waiting is a decision. And it is often the most expensive one.

The Illusion of “Perfect Timing”

Let’s start with a real scenario.

A 28-year-old earning $12,000 a month.

Strong income. High borrowing capacity. Stable career.

On paper, this person should already be building a property portfolio.

Instead, he is stuck.

Not because he lacks money. But because he wants to avoid making the wrong move.

Should he buy a 2-bedroom or stretch for a 3-bedroom? Should he wait for interest rates to fall? Should he invest in stocks first?

So he does what most people do.

He waits.

Why Waiting Feels Smart (But Isn’t)

Waiting gives you the illusion of control.

You tell yourself:

“I’m gathering more data.” “I’m being cautious.” “I’m avoiding risk.”

But in reality, you are doing something else.

You are delaying exposure to growth.

And in Singapore’s property market, that delay has a cost.

A very real one.

The Moving Walkway Problem

Think of the property market like a moving walkway at the airport.

If you stand still, you don’t stay in the same position.

You move backwards.

Why?

Because while you wait:

- Property prices continue to trend upward

- Your cash loses purchasing power due to inflation

- Entry prices increase faster than your savings

So even though you feel “safe” holding cash…

You are quietly losing ground.

The Hidden Cost of Inaction

Let’s break this down logically.

If you delay your purchase by 3–5 years:

- You miss capital appreciation

- You miss principal paydown (forced savings)

- You enter at a higher price point later

This is what most people don’t calculate.

They only think about:

“What if I buy and prices drop?”

But they never ask:

“What if I don’t buy and prices keep rising?”

That second scenario is far more common.

The 6-Figure Mistake Most Buyers Make

Here’s where the math becomes undeniable.

Scenario A: You Invest in Stocks

You put $250,000 into equities.

Market grows at 5%.

You make: → ~$12,500 per year

Good return.

Scenario B: You Buy Property

You use $250,000 as a 25% downpayment.

You control a $1,000,000 asset.

Property grows at just 3%.

You make: → $30,000 per year

That is more than double.

Why?

Because of one word:

Leverage.

Property allows you to use the bank’s money to amplify your returns.

Stocks do not.

The Real Advantage Isn’t Growth. It’s Scale.

This is the key insight most people miss.

Stocks may grow faster in percentage terms.

But property grows on a much larger base.

That difference compounds over time.

And that is how delays turn into:

$100K. $200K. Even $500K opportunity losses.

The Real Enemy: Lifestyle Inflation

Here’s the uncomfortable truth.

Most high-income earners don’t fail because they earn too little.

They fail because they spend too much.

At $12K/month, lifestyle creep kicks in fast:

- Car upgrades

- Luxury travel

- Dining habits

- Subscriptions and recurring costs

You feel rich.

But your liquidity tells a different story.

The Brutal Truth About Property Entry

Property does not care about your income.

It cares about your capital.

To enter the market, you need:

- Downpayment

- Stamp duty

- Legal costs

That’s often $300K–$500K upfront.

If your lifestyle is absorbing your cash flow…

You will never reach that threshold.

The Smart Players Think Differently

They don’t just earn more.

They optimise capital.

Strategy 1: Kill Inefficient Cash Drains

One overlooked example:

Insurance.

Many young professionals overpay for whole-life policies.

Switching to term insurance can free up:

→ $300–$500/month

Over 5 years:

→ $20K–$30K redirected into property capital

Strategy 2: Family Portfolio Structuring

This is rarely discussed openly.

But it is happening everywhere.

Families use portfolio splitting to avoid Additional Buyer Stamp Duty (ABSD).

Instead of parents buying a second property:

They fund the child’s first property.

Why?

Because:

- First property = no ABSD

- Second property = up to 20% tax

On a $1M property, that’s $200K saved.

Rent vs Buy. The Truth Nobody Tells You

Let’s be clear.

Renting is not “wrong”.

In the short term, it can even make sense.

But over 5–10 years, the math shifts dramatically.

Renting:

- 100% expense

- No equity

- Rent increases over time

Buying:

- Partial expense (interest)

- Partial savings (principal)

- Asset appreciation

Example:

$4,000/month rent × 5 years = $240,000 gone

Versus:

Owning → you build equity + benefit from appreciation

The Real Risk Isn’t Buying

It’s staying out of the game.

Too many people try to:

- Time the market

- Wait for crashes

- Predict interest rates

Let’s be honest.

Even institutions fail at this.

So what makes you think you can do it consistently?

The Truth About Property Success

It is not about perfect timing.

It is about:

- Entering early

- Holding long

- Leveraging correctly

The Core Principle

You are not buying a house.

You are buying:

- Leverage

- Time

- Exposure to growth

Final Thought

Every year you wait:

- Prices adjust

- Opportunities shift

- Entry becomes harder

You think you are avoiding risk.

But you are actually accepting a different one.

The risk of permanent delay.

If you are currently:

- Earning $8K–$15K/month

- Unsure whether to buy now or wait

- Deciding between 2-bed vs 3-bed

- Or stuck calculating endlessly

You are exactly the profile at risk of this “waiting trap”.

Send me a message with the word “MOVE”.

I will share with you:

- A personalised entry strategy

- Cash flow breakdown

- Risk vs return comparison

- Exit timeline planning

No fluff. Just numbers and strategy.

Because in Singapore property…

The biggest mistake is not buying the wrong unit.

It is waiting so long that the right unit is no longer affordable.

#M #ThisIsM #ThisisMMikeChin #Propnex #MAssociate #Msingaporeproperty #AIForRealtors #RealEstate #PropertyForSale #InvestIngRealEstate #RealEstateInvestment #HomeBuyers #PropertyInvestment #DreamHome #HouseGoals #PropertyMarket #RealEstateLife #RealEstateExpert #HomesForSale #InvestIngProperty #RealEstateDevelopment #NewHome #OpenHouse #RealEstateSingapore #CondoLife #LuxuryLiving #HomeSweetHome #RealEstateTips #RealEstateInvestor #businessmentorship